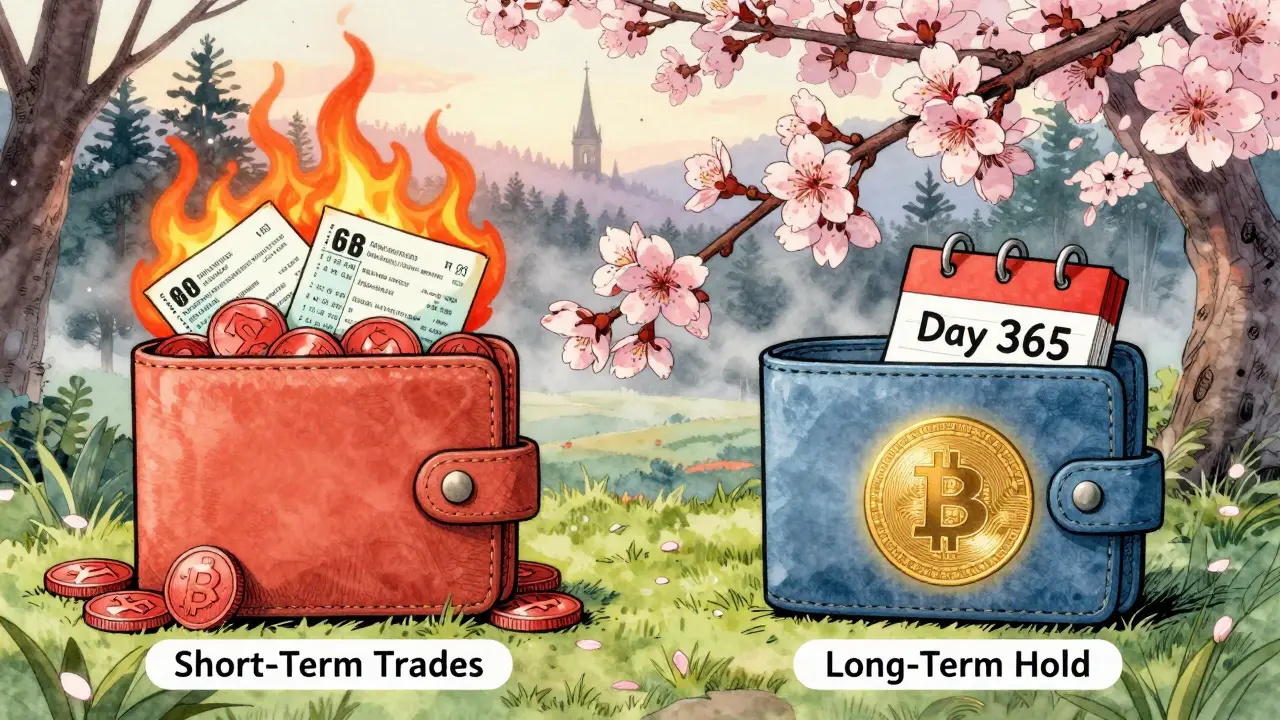

If you hold Bitcoin or other cryptocurrencies in Germany and you’ve kept them for over a year, you might not owe a single euro in taxes when you sell. That’s not a rumor. It’s the law. Since March 2025, Germany has officially confirmed that crypto gains are completely tax-free if you hold your assets for at least 365 days. This isn’t just a loophole - it’s a structured, government-backed exemption that’s reshaping how people invest in digital assets across Europe.

How the 12-Month Rule Actually Works

The rule is simple: buy Bitcoin, Ethereum, or any other recognized cryptocurrency. Hold it for exactly 365 days - not 364, not 366. The clock starts the moment you acquire it. If you sell, trade, or even spend it after that date, any profit you make is tax-free. No reporting. No paperwork. No tax bill.

This applies to all types of crypto transactions: selling for euros, swapping one coin for another, or using crypto to pay for goods and services. Even if you made €50,000 in profit, you keep it all. The German Federal Central Tax Office (BZSt) doesn’t care how big the gain is - only how long you held it.

But here’s the catch: if you sell before the 12-month mark, you’re taxed. And the rates are steep. Short-term gains (under 365 days) are treated as ordinary income. That means your profit gets added to your yearly earnings and taxed at Germany’s progressive income tax rates - from 14% up to 45%. Add in the 5.5% Solidarity Tax, and you could be paying up to 47.5% in taxes on your crypto profits. That’s more than double what most countries charge on capital gains.

The €1,000 Short-Term Exemption - A Trap for Beginners

There’s a small buffer for small-time traders: if your total net crypto gains in a year are under €1,000, you don’t have to report anything. Sounds nice, right? But this isn’t a free pass. It’s a trap.

Let’s say you bought Ethereum in January and sold it in October for a €900 profit. You’re fine. But if you bought another coin in February and sold it in November for a €200 profit, you’ve now hit €1,100 in total gains. Suddenly, all your gains for the year become taxable - not just the €100 over the limit. The system doesn’t let you pick and choose which trades to report. It’s all or nothing.

And if you’re actively trading? This rule works against you. The German tax system uses FIFO (First-In-First-Out) accounting. That means if you bought Bitcoin in 2021 and again in 2025, and you sell some in 2026, the tax office assumes you sold the oldest coins first. If those were bought more than a year ago, you’re safe. But if you mixed short-term buys with long-term ones in the same wallet, you could accidentally trigger taxes on assets you thought were exempt.

What Counts as a Taxable Event?

Not all crypto activity is treated the same. Here’s what triggers taxes:

- Selling crypto for euros or another currency - taxable if under 12 months

- Swapping one crypto for another - treated as a sale, so same rules apply

- Using crypto to buy goods or services - even buying coffee with Bitcoin counts as a disposal

- Receiving staking or mining rewards - taxed as income when received, but if you hold them for 12 months, then sell, the profit is tax-free

- Yield farming or DeFi liquidity pool rewards - taxed immediately upon receipt, no exemption

Staking rewards are especially tricky. You pay income tax on them the day you get them. But if you hold those rewards for a full year before selling them, the profit you make from that sale is tax-free. It’s a two-step tax process: pay upfront on the reward, then enjoy tax-free gains later.

How Germany Compares to the Rest of Europe

Most of Europe taxes crypto like stocks. France? Flat 30% tax, no matter how long you hold. The UK? You get a £6,000 annual allowance, but anything over that is taxed. The Netherlands? Full income tax rates on short-term gains, with no exemption.

Germany stands out because it treats crypto as private money, not an investment asset. That’s why it’s one of only two EU countries - alongside Portugal - that lets you keep 100% of your gains after a year. Portugal used to be better (only 28 days needed), but they tightened rules in 2024. Now, Germany’s 12-month rule is the most generous in the bloc.

But there’s a looming threat. The EU is pushing a new rule called DAC8, set to roll out in 2027. It could force all member states to adopt a standard 15% capital gains tax after a 365-day holding period. If that happens, Germany’s current system - with its full exemption - might disappear. That’s why many investors are rushing to lock in their gains before 2027.

Real Stories from German Crypto Holders

One Reddit user, 'CryptoHODLer87', held 1.2 BTC for 366 days, then sold. He saved €8,450 in taxes. He didn’t hire a tax advisor. He just waited. Another user, 'DayTraderDE', sold ETH after 353 days - 12 hours too early. He got hit with €3,200 in taxes. He didn’t realize the system tracks time down to the minute.

Most people who get it right use separate wallets. One wallet for short-term trades. Another for long-term holds. That way, they never accidentally mix up purchase dates. Tools like Koinly and BitcoinSteuer help track exact acquisition times. But even then, 68% of users say they still double-check timestamps manually.

One common tip? Always screenshot your transaction details. The date, time, amount, and exchange. If the tax office ever asks, you need proof.

What You Must Do to Stay Compliant

Germany doesn’t require you to file a tax return if your gains are under €1,000 and all your holdings are over 12 months. But if you sell anything before the year is up - even once - you must report everything.

You file through the Elster online portal. Paper forms are allowed, but the tax office strongly discourages them. The system is built for digital submissions. If you’re using multiple exchanges - like Coinbase, Kraken, or Bison - you need to export transaction histories from each one and combine them. The Elster crypto module is better than it was in 2023, but it still can’t auto-calculate FIFO. Most people use third-party software to generate the report, then upload it.

Remember: you can’t pick which coins to sell. FIFO is mandatory. If you bought 0.5 BTC in January 2023 and another 0.5 BTC in January 2025, and you sell 0.3 BTC in March 2026, the system assumes you sold the 2023 coins first - even if you meant to sell the newer ones. That’s why separate wallets matter.

What’s Coming Next?

The German government isn’t planning to change the 12-month rule anytime soon. In fact, they clarified it further in March 2025, confirming that NFTs, stablecoins, and DeFi rewards follow the same rules.

But the EU is watching. By 2027, DAC8 could force Germany to adopt a uniform tax rate across the bloc. If that happens, the exemption might vanish - or at least be capped at 15%. Experts at Deloitte estimate a 60% chance of this change occurring. That’s why many German investors are accelerating their plans to cash out before then.

Right now, Germany is the most crypto-friendly country in Europe. But that advantage won’t last forever. If you’re holding crypto there, the message is clear: wait 365 days. Then act.

Do I need to report crypto if I held it for over a year and didn’t sell?

No. If you never sold, swapped, or spent your crypto, there’s no taxable event. Germany only taxes you when you dispose of the asset. Holding it for years without selling means zero tax liability.

Can I avoid taxes by gifting crypto to someone else?

No. Gifting crypto to another person counts as a disposal. You’ll owe tax on any gain up to the value of the gift if you held it less than 12 months. If you held it longer, the gift is tax-free for you - but the recipient starts their own 12-month clock when they receive it.

What if I bought crypto on multiple exchanges? Do I need to track each one?

Yes. Each purchase, regardless of exchange, has its own acquisition date. You must track all of them. Mixing trades from different platforms in the same wallet can trigger FIFO errors and accidental taxation. Use separate wallets or tax software that imports data from all your exchanges.

Are stablecoins like USDT or USDC taxed the same as Bitcoin?

Yes. Germany treats stablecoins as cryptocurrencies under Section 23 EStG. Swapping euros for USDT counts as a purchase. Swapping USDT for Bitcoin counts as a sale. The 12-month rule applies the same way. Even if the price doesn’t move, the transaction itself triggers tax rules.

What happens if I move out of Germany before the 12 months are up?

You’re still liable for German taxes on any crypto sold while you were a resident. The tax obligation is tied to your residency status at the time of the sale. If you move after 11 months and sell 30 days later in another country, Germany still claims the tax. You’ll need to file a German tax return for that year.

Michael Suttle

March 12, 2026 AT 04:53 AMThis is total BS. 🤡 Germany's 'tax-free' crypto rule? It's a trap set by the ECB to lure in dumb money before DAC8 drops. They want you to pile in, then BAM - EU-wide tax clawback in 2027. They're not helping you - they're harvesting your capital. I've seen this movie. It ends with your wallet empty and your trust shattered. 🚨

Julie Tomek

March 13, 2026 AT 17:09 PMI appreciate the thorough breakdown of Germany’s crypto tax framework. It is indeed one of the most favorable regulatory environments in the European Union. The 12-month holding period creates a clear, predictable structure for long-term investors. However, I must emphasize that while the exemption is generous, it requires meticulous record-keeping. Many individuals overlook the importance of documenting acquisition timestamps across exchanges, which can lead to unintended tax consequences. I strongly recommend using a dedicated tax software platform, such as Koinly or BitcoinSteuer, and maintaining separate wallets for short-term and long-term holdings. This level of diligence transforms a complex compliance burden into a manageable, even empowering, financial practice.

Brandon Kaufman

March 14, 2026 AT 13:45 PMI’ve been holding my BTC since 2022. Just sold 0.3 last week - tax-free. Honestly? It felt weird. Like I won a game nobody else knew they were playing. The hardest part wasn’t the waiting - it was the anxiety of thinking I messed up the dates. I took screenshots of every trade. Even the tiny ones. You don’t want to be the guy who got hit with €3k because he sold 12 hours early. Stay sharp. And yeah, separate wallets. Seriously.

Craig Gregory

March 15, 2026 AT 16:54 PMThe notion that this is a ‘structured exemption’ is a performative illusion. The German state doesn’t grant tax relief - it manipulates behavioral incentives. By offering a 12-month window, they engineer herd behavior. Investors become passive holders, not active participants in the market. This isn’t policy - it’s psychological conditioning. And when DAC8 arrives, the entire architecture collapses under its own weight. The system is designed to fail. You’re not winning. You’re being farmed.

Anshita Koul

March 17, 2026 AT 09:33 AMI find this entire framework fascinating - not because it's generous, but because it reveals a deeper philosophical truth: time, not technology, is the ultimate validator of value. In a world obsessed with volatility, Germany says: wait. Let the market settle. Let emotion fade. Let the noise die down. And then - only then - is profit not a gamble, but a reward. The 12-month rule is a meditation. It’s not about avoiding tax - it’s about avoiding chaos. I wish more systems, financial or otherwise, had such wisdom.

Douglas Anderson

March 17, 2026 AT 10:33 AMI used to think the €1,000 exemption was a gift. Then I lost €2,100 because I mixed trades. The FIFO system is brutal. I now have three wallets: one for swaps (short-term), one for holds (long-term), and one for staking rewards (which I treat like a separate asset). It’s annoying, but it works. If you’re trading at all, use Koinly. It’s not perfect, but it’s better than crying over a tax bill you didn’t mean to trigger.

Tina Keller

March 18, 2026 AT 02:27 AMGermany’s move feels like a quiet rebellion - like a grandparent who says, ‘You don’t need to prove your worth to the system.’ They’re not treating crypto as a commodity. They’re treating it like cash. And honestly? That’s radical. In a world where everything is tracked, taxed, and monetized, this is a breath of fresh air. I don’t care if DAC8 comes - this rule gave people peace. That’s worth more than any tax code. I’m proud of them.

vasantharaj Rajagopal

March 18, 2026 AT 18:42 PMThe core issue lies in the conflation of disposal events under Section 23 EStG. While the 12-month holding period provides a de facto capital gains exemption, the treatment of stablecoin swaps as taxable events introduces a significant friction point in DeFi ecosystems. The FIFO methodology, while administratively efficient, is fundamentally incompatible with UTXO-based accounting models prevalent in non-custodial wallets. This creates a structural asymmetry between retail participants and institutional actors who employ custodial solutions with integrated tax engines.

ann neumann

March 20, 2026 AT 17:06 PMThey’re lying. I know it. I’ve seen the emails. The BZSt doesn’t care about your timestamps. They’re watching. They’re waiting. They already have your wallet addresses from Coinbase. They’re building a database. You think you’re safe? You’re not. One day, they’ll come for you. And when they do, they’ll say, ‘You had 366 days. But we counted the leap second.’ They’re not here to help you. They’re here to take it all. I’m moving my coins to Switzerland. Pray for me.

William Montgomery

March 21, 2026 AT 02:23 AMYou’re not ‘saving’ money. You’re avoiding responsibility. If you made €50k, you should pay taxes. This rule encourages laziness. It’s not freedom - it’s evasion dressed up as policy. And don’t pretend you’re some smart investor. You’re just gaming a loophole. The system’s not broken - you are.