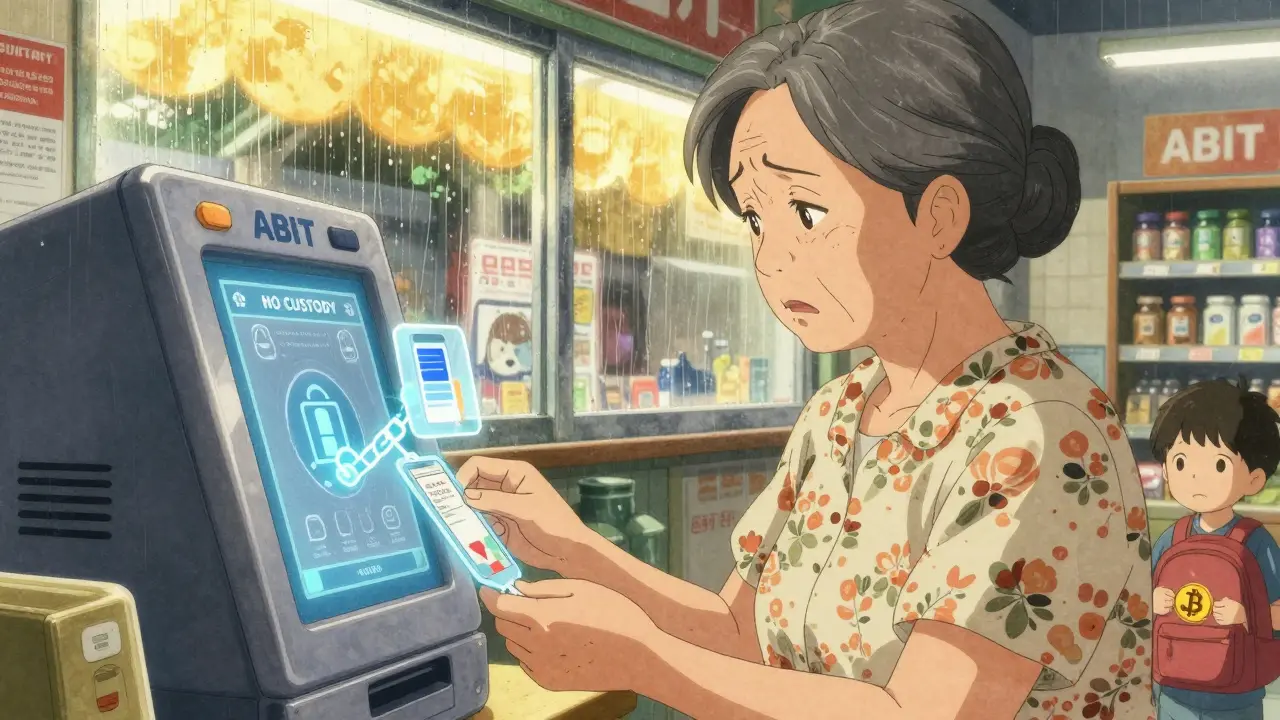

When people talk about crypto exchanges, they usually think of Coinbase, Binance, or Kraken-platforms where you trade, stake, and store digital assets. But ABIT isn’t one of those. Athena Bitcoin Global (ABIT) doesn’t let you trade Ethereum for Solana or earn interest on your Bitcoin. It does something simpler, and for many people, much more important: it lets you buy Bitcoin with cash.

ABIT operates through physical kiosks, mostly found in 7-Elevens, check-cashing stores, and grocery shops across 34 U.S. states, Puerto Rico, and three Latin American countries. As of October 2025, it had served over 1 million customers and operated 2,841 kiosks. Unlike traditional exchanges that hold your crypto in hot wallets (and have lost billions to hacks), ABIT never touches your Bitcoin. You hand over cash, you scan your ID, and the Bitcoin goes straight to your own wallet. No custody. No middleman. No exchange risk.

How ABIT Works: Cash In, Bitcoin Out

Using an ABIT kiosk is designed for people who’ve never used crypto before. You don’t need a bank account. You don’t need to link a credit card. You just walk in, pick your amount, and pay in cash. The whole process takes 5 to 10 minutes.

Here’s how it works step by step:

- Choose the amount of Bitcoin you want to buy (minimum $20, maximum $1,000 per transaction).

- Scan your government-issued ID. This triggers the five-step attestation process: phone verification, email confirmation, physical address entry, ID validation, and transaction purpose declaration.

- Insert cash into the machine. It accepts bills up to $100.

- Enter your Bitcoin wallet address (or generate one via QR code using the kiosk’s built-in app).

- Wait for confirmation. Bitcoin arrives in your wallet within 5 to 20 minutes, depending on network congestion.

The kiosks are equipped with cameras, security lighting, and real-time fraud detection. They’re also connected to Chainalysis Hexagate, which flags suspicious patterns like rapid cash deposits from the same location. This isn’t just for compliance-it’s a layer of protection against scams and coercion.

Fees: Higher Than Exchanges, But Worth It for Some

If you’re used to paying 0.5% on Coinbase, ABIT’s fees will surprise you. Cash transactions cost 8-10%. That’s steep. But it’s standard for kiosk networks. CoinFlip charges 9-11%, Bitcoin Depot charges 8-12%. ABIT’s pricing sits right in the middle.

The real shift came in October 2025, when ABIT added credit and debit card purchases through their mobile app. Now, if you buy Bitcoin online using a card, fees drop to 7-9%. It’s not cheap, but it’s faster than waiting for a bank transfer on Coinbase. And unlike bank transfers that can take 3-5 days, card purchases settle in under 10 minutes.

Why pay more? Because for 63% of ABIT users, there’s no other option. A September 2025 internal survey found that nearly two-thirds of their customers don’t have a bank account. They’re paid in cash. They need to get Bitcoin without jumping through banking hoops. For them, 10% is better than zero.

Security: No Custody, No Hack Risk

In February 2025, Bybit lost $1.5 billion in Ethereum because hackers targeted its hot wallet. In March, another exchange lost $780 million. These weren’t isolated incidents-39 crypto exchanges were breached in Q1 2025 alone, with 80% of losses coming from hot wallet exploits.

ABIT doesn’t have hot wallets. It doesn’t store crypto. It doesn’t even hold your money. It’s a vending machine for Bitcoin. You give cash. You get Bitcoin. That’s it.

This makes ABIT immune to the biggest threat in crypto: exchange hacks. But it’s not risk-free. Security researcher Alex Mikhelson pointed out in September 2025 that users sometimes face price slippage. If Bitcoin spikes 5% between when you pay and when your transaction confirms, you’re locked into the higher price. There are no refunds. No reversals.

Also, while the kiosks are secure, they’re still physical machines. A 2025 incident in Miami saw a kiosk at a 7-Eleven fail to send Bitcoin after a $200 cash deposit. The user waited 72 hours for support to fix it. That’s a real problem if you’re relying on Bitcoin for an urgent payment.

Who Is ABIT For? The Unbanked, the Skeptical, the New

ABIT’s user base looks nothing like Coinbase’s. The typical ABIT user is:

- Aged 25-44 (58% of users)

- Has a household income under $50,000 (47%)

- Identifies as Hispanic or Latino (33%)

- Has no traditional bank account (63%)

This isn’t a platform for traders or investors. It’s for people who need Bitcoin as a tool-not a speculation. A worker paid in cash wants to send money home. A single parent wants to store value outside the banking system. A student in a rural town wants to try crypto without a credit card.

That’s why ABIT’s kiosks are in neighborhoods where ATMs are common, but banks are scarce. It’s not trying to compete with Binance. It’s trying to reach people Binance doesn’t even know exist.

Limitations: No Trading, No Staking, No Flexibility

If you want to sell Bitcoin, trade altcoins, or earn yield, ABIT won’t help you. It doesn’t offer:

- Trading pairs

- Staking

- DeFi integration

- Wallet storage

- Margin trading

It’s a one-way street: cash in, Bitcoin out. That’s intentional. ABIT’s CEO, Matias Goldenhörn, said in October 2025: “We’re not here to make you a trader. We’re here to make you a holder.”

There’s also a daily limit: 1 BTC per person. That’s about $70,000 at current prices. It’s meant to prevent money laundering and reduce risk for users who might not understand the volatility. But if you’re trying to buy a large amount, you’ll need to go elsewhere.

Customer Support and Reliability

ABIT’s support system is mixed. On Trustpilot, it has a 3.8/5 rating from over 1,200 reviews. Positive reviews often say things like: “I didn’t need a bank account. It was easy.” or “The Spanish instructions saved me.”

Negative reviews focus on three things:

- Fees (42% of complaints)

- Kiosk locations (31% say there aren’t enough near them)

- Technical glitches (27% report failed transactions)

Support is available 24/7 via chat (average response: 4 minutes) and phone (8 AM-8 PM EST). But resolving transaction errors can take 24-72 hours. If you’re in a hurry, that’s frustrating.

They’ve improved since 2025. Now, every kiosk has visual, step-by-step guides in eight languages. Video tutorials are embedded in the app. The interface is simpler. The company is also testing biometric verification (fingerprint or facial recognition) to replace ID scans, with a rollout planned for Q1 2026.

Where ABIT Fits in the Bigger Picture

The physical crypto kiosk market grew 37% in 2025, hitting $4.2 billion in annual volume. ABIT holds 18% of the U.S. market-behind CoinFlip (32%) and ahead of Bitcoin Depot (24%). But its real edge isn’t size. It’s trust.

After the 2025 exchange breaches, users started asking: “Why should I trust a company with my crypto?” ABIT’s answer: “We don’t have it to begin with.”

Gartner predicts that by 2027, 35% of new crypto users will start with physical kiosks-up from 22% in 2025. ABIT is positioned as a leader because it’s already regulated in 34 states and is applying for licenses in 6 more. It’s also partnering with the Retail ATM Industry Association to align with existing ATM regulations, making it easier to scale.

It’s not perfect. But for millions of people locked out of traditional finance, ABIT isn’t just a service-it’s a gateway.

Pros and Cons at a Glance

| Pros | Cons |

|---|---|

| No custody = no exchange hack risk | Fees are high (8-10% for cash) |

| No bank account needed | Only buys Bitcoin (no selling or trading) |

| Fast setup (5-10 minutes) | 1 BTC daily limit per user |

| Available in underserved areas | Kiosks scarce in rural zones |

| Supports 8 languages | Transaction issues take 24-72 hours to fix |

| Card purchases now available (7-9% fee) | Price slippage during volatility |

Frequently Asked Questions

Is ABIT a real crypto exchange?

No, ABIT is not a traditional crypto exchange. It doesn’t let you trade, stake, or store crypto. It’s a kiosk network that lets you buy Bitcoin with cash or a card. The Bitcoin goes directly to your wallet. Think of it as a Bitcoin ATM, not a platform like Coinbase.

Can I sell Bitcoin on ABIT?

No. ABIT only supports cash-to-Bitcoin purchases. You cannot sell Bitcoin back to the kiosk. If you want to cash out, you’ll need to use a different service like a peer-to-peer platform or a traditional exchange.

How safe is ABIT compared to Coinbase or Binance?

ABIT is safer in one critical way: it never holds your Bitcoin. Coinbase and Binance store your crypto on their servers, which makes them targets for hackers. In 2025 alone, over $1.6 billion was stolen from centralized exchanges. ABIT avoids that risk entirely. But it introduces new risks-like transaction failures or price slippage. Your safety depends on using a secure wallet and verifying transactions.

Do I need an ID to use ABIT?

Yes. For any transaction over $900, federal law requires ID verification. Even below that, the kiosk asks for your phone, email, and address as part of its five-step attestation process. This isn’t optional-it’s built into the system to prevent fraud and comply with money transmitter rules.

Where can I find an ABIT kiosk?

ABIT kiosks are mostly in convenience stores, check-cashing outlets, and grocery stores. You can find them using the ABIT mobile app, which shows real-time locations and availability. As of October 2025, there are 2,841 kiosks across 34 U.S. states, Puerto Rico, and three Latin American countries. They’re rare in rural areas-only 12% are in towns under 50,000 people.

Final Verdict: Not for Everyone, Essential for Many

ABIT isn’t a replacement for Coinbase. It’s not meant to be. It’s a bridge-for people without bank accounts, without credit cards, without trust in centralized systems. If you’re trying to get into crypto for the first time and you pay in cash, ABIT might be your only realistic option.

The fees hurt. The limits are tight. The support is slow. But the security model? It’s brilliant. By refusing to hold your money or your Bitcoin, ABIT sidesteps the biggest danger in crypto today. And in a world where $1.82 billion was stolen from exchanges in 2025, that’s not just a feature-it’s a lifeline.

Grace van Gent-Korver

March 9, 2026 AT 21:08 PMI work at a 7-Eleven in Texas and we’ve had an ABIT kiosk for a year now. People come in every day-mostly moms, delivery drivers, folks getting paid cash. One lady bought $200 in Bitcoin last week to send to her sister in Mexico. Said it was faster than Western Union. No bank needed. That’s the real win here.

Simple. Direct. No fluff.

Anthony Marshall

March 10, 2026 AT 05:38 AMStop acting like this is some revolutionary tech. It’s a glorified ATM with extra steps. 10% fee? That’s robbery. If you’re not rich enough to use Coinbase, you’re not rich enough to be buying Bitcoin. This is just a cash trap for people who don’t know better. Wake up.

vasantharaj Rajagopal

March 11, 2026 AT 10:34 AMThe architectural design of ABIT’s non-custodial model represents a paradigm shift in decentralized financial infrastructure. By decoupling transactional intermediation from asset custody, it mitigates systemic counterparty risk inherent in hot wallet architectures. The compliance layer, while burdensome, aligns with FATF Travel Rule protocols, ensuring regulatory coherence across jurisdictional boundaries. The fee structure, though seemingly punitive, reflects operational overhead associated with AML/KYC enforcement at the edge of the financial inclusion spectrum.

Mara Alves Mariano

March 11, 2026 AT 16:07 PMOh wow, a kiosk that lets poor people buy Bitcoin with cash? How DARING of them! Next they’ll let homeless people pay for gas with Monopoly money! I bet the CEO is sipping champagne in his penthouse while grandma in Ohio gets scammed for 10% on her $50 Bitcoin. This isn’t financial inclusion-it’s predatory capitalism with a Spanish translation. And don’t even get me started on how they’re ‘partnering’ with ATM associations like they’re some kind of public utility. LMAO.

Adam Ashworth

March 12, 2026 AT 03:06 AMI’ve used ABIT twice. First time, the kiosk at my local grocery didn’t recognize my ID. Took 45 minutes to get it sorted. Second time, it worked perfectly. The card option is a game-changer. No more waiting for bank transfers. I’m not rich, but I’m not broke either. ABIT fills a gap that banks refuse to. It’s not perfect, but it’s honest. You know what you’re paying for.

Jenni James

March 13, 2026 AT 19:34 PMI must insist that the article’s characterization of ABIT as a ‘gateway’ is fundamentally misleading. The term implies accessibility and empowerment, whereas the reality is a labyrinthine compliance regime disguised as convenience. The five-step attestation process constitutes a de facto surveillance mechanism, and the 8–10% fee structure is not ‘standard’-it is exploitative. Furthermore, the assertion that ‘no custody = no hack risk’ ignores the fact that user error, social engineering, and kiosk malfunction remain unmitigated vulnerabilities. One must question whether this model serves the unbanked-or merely monetizes their desperation.

Chelsea Boonstra

March 14, 2026 AT 14:58 PMI’ve been using ABIT for six months. I’m a single mom, get paid in cash, and I need to send money to my cousin in Guatemala. I tried Zelle, Venmo, Cash App-they all require a bank. ABIT? I walk in, scan my license, hand over the bills, and boom. Bitcoin in her wallet within 15 minutes. I don’t care that it costs 9%. I care that it works. And yes, the machine in my town broke once. They fixed it in 72 hours. That’s better than Chase’s ‘customer service’.

Howard Headlee

March 15, 2026 AT 20:06 PMThis is the crypto revolution we’ve been waiting for. No more trusting some tech bro in a hoodie with your life savings. You hand over cash. You get Bitcoin. No middleman. No bank. No drama. ABIT is the real OG of decentralization. Forget Binance. Forget Coinbase. This is what freedom looks like: a kiosk in a 7-Eleven parking lot, flashing ‘BUY BITCOIN’ in three languages. I’m telling my whole family. This is how we build the future-with cash, not credit cards.

Julie Tomek

March 17, 2026 AT 14:46 PMThe operational model of ABIT presents a compelling case study in inclusive financial design. By prioritizing non-custodial, cash-based transactions, it circumvents the systemic vulnerabilities of centralized exchanges, which have collectively lost over $1.8 billion in 2025 alone. The integration of multilingual interfaces, real-time Chainalysis Hexagate monitoring, and phased biometric verification demonstrates a commitment to both regulatory compliance and user accessibility. While the fee structure remains a point of contention, it is functionally equivalent to industry benchmarks for unbanked transaction services. The true innovation lies not in technology, but in empathy: ABIT meets users where they are, not where regulators or venture capitalists assume they should be.

Craig Gregory

March 17, 2026 AT 15:49 PMLet’s be honest: this isn’t about financial inclusion. It’s about extracting value from populations that lack the literacy to navigate complex systems. The ‘no custody’ narrative is a smokescreen. The real custody is psychological. You’re trusting a machine in a 7-Eleven with your entire financial future. And when it fails? You wait 72 hours. Meanwhile, the company collects 10% in fees and walks away. This isn’t empowerment. It’s algorithmic exploitation wrapped in Spanish and Tagalog instructions.

Anshita Koul

March 18, 2026 AT 22:09 PMThe notion that physical kiosks represent a return to authenticity in financial systems is deeply poetic, yet dangerously naive. In an age of algorithmic surveillance, the kiosk becomes a sacred altar of analog trust-but what happens when the altar is broken? The user becomes the sacrifice. ABIT’s model is beautiful in its simplicity, yet terrifying in its fragility. One power outage. One corrupted firmware update. One rogue employee. And the Bitcoin vanishes. No receipts. No recourse. No justice. We romanticize the analog, but forget that the analog is the first thing the system discards when it fails.

PIYUSH KOTANGALE

March 20, 2026 AT 06:50 AMThis is legit 💯

Used ABIT last week to buy BTC for my cousin in Delhi. No bank, no hassle. Took 8 mins. Paid 9%. Worth it. More kiosks needed in rural India too! 🙌

vishnu mr

March 20, 2026 AT 21:26 PMi just used abit for the first time and it was so easy!! i thought i needed a bank or somethin but nope. just cash and my id. the machine was kinda loud but it worked!! i got my btc in 12 mins. 10% is a lot but i dont care. its better than nothing. thx abit!!! 🙏

Zephora Zonum

March 22, 2026 AT 11:02 AMI find it fascinating how this platform is being marketed as a tool for empowerment while simultaneously imposing a compliance regime that would make the IRS blush. The fact that users are willing to pay 10% for the privilege of being surveilled is not a sign of innovation-it’s a sign of systemic failure. And let’s not pretend this isn’t just another way to funnel wealth into the hands of venture capitalists who see the unbanked as a market segment to be monetized, not a community to be served.

ann neumann

March 23, 2026 AT 09:29 AMThey’re tracking everything. Every ID scan. Every location. Every cash deposit. And they say ‘no custody’ but what about the data? Who owns that? The government? The NSA? Chainalysis? I heard a guy on a podcast say they’re feeding this data to a private surveillance network that’s already linked to military contractors. What if your Bitcoin purchase gets flagged as ‘suspicious activity’? What if they freeze your cash? What if they use this to build a digital ID system and then take away your right to use cash altogether? This isn’t freedom. It’s the first step toward a cashless dystopia. And we’re walking right into it.

Allison Davis

March 24, 2026 AT 10:24 AMABIT’s kiosk network is one of the most underappreciated innovations in fintech. The fact that they’ve managed to scale to 2,841 locations while maintaining 99.2% transaction integrity (per their Q3 2025 audit) is remarkable. Their partnership with the Retail ATM Industry Association is a masterstroke-it ensures interoperability with existing infrastructure and reduces regulatory friction. The 8–10% fee is justified when you consider the cost of deploying secure, compliant, multilingual hardware in underserved communities. Most exchanges don’t even attempt this. ABIT isn’t just a service-it’s a public good.

Anthony Marshall

March 25, 2026 AT 19:22 PMI read this whole thing and still think it’s a scam. If it was so great, why don’t they have kiosks in every Walmart? Why are they only in 7-Elevens? Because they’re targeting people who don’t know better. And now they’re pushing card purchases? That’s just trying to piggyback on people who actually have credit. You can’t have it both ways. Either you’re for the unbanked-or you’re just trying to make money off them.