Crypto Tax Calculator

Calculate Your Crypto Tax Liability

Enter your transaction details to see your capital gains tax calculation and how legal tax strategies could reduce your bill.

Tax Evasion Warning

Legal tax avoidance is smart financial planning. Illegal tax evasion is a federal crime. The IRS has tools to track your transactions through exchanges, blockchain analytics, and bank records. Do not attempt to hide or misreport crypto activity.

Legal Tax Reduction Strategies

Here's how you can reduce your tax bill legally:

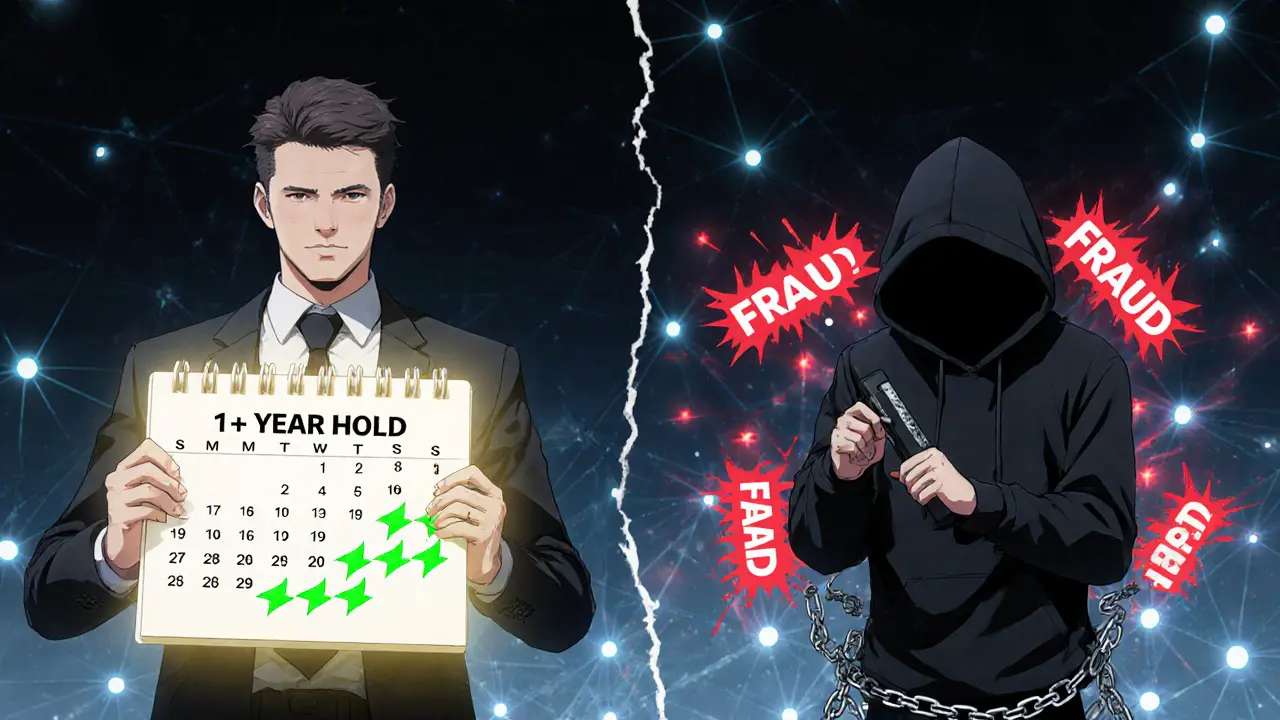

- Hold assets for over 1 year to qualify for lower long-term capital gains rates

- Use tax-loss harvesting to offset gains with losses up to $3,000 per year

- Gift crypto to family members within annual gift tax exclusion limits

- Consider holding crypto in a self-directed IRA for tax-deferred growth

- Document all transactions and keep records for at least 7 years

Many crypto holders think they can skip reporting their gains - after all, Bitcoin transactions feel anonymous. But here’s the truth: crypto tax evasion isn’t a loophole. It’s a federal crime. And the IRS isn’t waiting for you to make a mistake. They’ve already got your data.

What’s the real difference between avoidance and evasion?

Legal tax avoidance means using the rules to pay less. Think of it like maxing out your 401(k) to lower your taxable income. You’re not hiding anything. You’re just playing by the book. Tax evasion is lying. It’s hiding crypto sales, pretending staking rewards aren’t income, or using mixers to scrub your transaction history. It’s fraud. And the penalties? Fines up to $250,000. Jail time. A criminal record. The difference isn’t subtle. One is smart planning. The other is stealing from the government.When does crypto trigger a tax event?

You don’t just owe taxes when you sell Bitcoin for dollars. The IRS treats crypto like property. Every time you:- Sell crypto for fiat (USD, EUR, etc.)

- Trade one crypto for another (BTC for ETH)

- Use crypto to buy goods or services (coffee, a laptop, a NFT)

- Receive crypto as payment (salary, freelance work, airdrops)

- Earn staking or mining rewards

Legal ways to reduce your crypto tax bill

You don’t have to pay the full amount. Here’s what works:Hold for over a year

Short-term capital gains (assets held less than a year) are taxed at your regular income rate - up to 37%. Long-term gains (held over a year) are taxed at 0%, 15%, or 20%, depending on your income. If you bought ETH in January 2024 and sell it in March 2025, you save thousands.Use tax-loss harvesting

If you own crypto that’s down in value, sell it. You can use the loss to offset gains from other trades. You can even deduct up to $3,000 in net losses against your regular income each year. Any extra losses roll forward to next year. Example: You made $8,000 in gains from selling Solana. You also sold Cardano at a $5,000 loss. You only pay tax on $3,000 in net gains. That’s a 62.5% reduction.Gift crypto to family

You can gift up to $19,000 per person per year (2025 limit) without triggering gift tax. The recipient inherits your cost basis. If they’re in a low-income bracket, they might pay 0% capital gains tax when they sell.Hold crypto in a retirement account

Some self-directed IRAs let you buy Bitcoin and Ethereum. Gains grow tax-free (Roth) or tax-deferred (Traditional). No reporting until you withdraw. But be careful - not all providers allow crypto, and fees can be high.Structure as a business

If you mine, stake, or trade crypto full-time, you might qualify as a business. That lets you deduct expenses: electricity, hardware, software, even home office space. You’ll pay self-employment tax, but you can also offset income with losses.How people get caught - even when they think they’re hidden

A 2021 study in Norway found that 88% of crypto holders didn’t report their holdings. That’s not because they’re clever. It’s because they didn’t know. But here’s the catch: crypto tax evasion is getting harder to get away with. Major exchanges like Coinbase, Binance, and Kraken now report to the IRS. Starting in 2026, all U.S. exchanges must issue Form 1099-DA - a new form that tracks every sale, trade, and transfer. The IRS will know exactly how much you made. Even decentralized exchanges (DEXs) aren’t safe anymore. Blockchain analytics firms like Chainalysis and Elliptic track wallet movements. If you ever used a KYC exchange - even once - your wallet is linked to your identity. The IRS sends letters. They audit. They subpoena bank records. If you transferred $10,000 from Binance to your bank account and didn’t report it? They’ll find it.

What tax evasion looks like in real life

Here’s what the IRS considers fraud:- Not reporting staking rewards from Coinbase or Kraken

- Claiming you “lost” your private keys to avoid reporting a $50,000 gain

- Using Monero or Tornado Cash to obscure transactions

- Filing a tax return that says “no crypto activity” while your wallet shows 200 trades

- Transferring crypto to a friend’s wallet to “hide” it

Who’s most at risk?

Data shows the biggest noncompliers are young, urban, male crypto traders. Not because they’re trying to cheat - but because they think taxes don’t apply to “digital money.” The average tax gap per noncomplier? Between $200 and $1,087. That’s not a fortune. But multiply that by millions of users? The IRS sees a $10 billion opportunity. They’re not going after everyone. They’re targeting the top 5% of traders - the ones with big gains, frequent activity, or transfers to offshore wallets. If you’re trading $10k+ per month? You’re on their radar.What you should do right now

Stop guessing. Start documenting.- Track every transaction: buy, sell, trade, gift, earn

- Record the date, amount, cost basis, and fair market value at time of transaction

- Use a crypto tax tool like Koinly, CoinTracker, or TokenTax - they connect to exchanges and auto-calculate gains

- Keep records for at least 7 years

- Consult a CPA who understands crypto - don’t rely on your general accountant

The future is transparent

Crypto isn’t going away. Taxes aren’t going away. The idea that you can trade anonymously and never pay tax is a myth built on ignorance. The blockchain is public. The IRS has tools. Exchanges are reporting. The game has changed. Legal tax avoidance? That’s still alive. Smart investors use it to keep more of their gains. They file on time. They keep records. They know the rules. Illegal evasion? That’s a one-way ticket to penalties, audits, and possibly prison. No one gets away with it forever. The choice isn’t about being rich or poor. It’s about being smart - or being reckless.What happens if you get caught?

If the IRS audits you and finds unreported crypto gains:- You’ll owe back taxes + interest (compounded daily)

- You’ll face a 20% accuracy-related penalty

- If they prove fraud, you’ll pay a 75% civil fraud penalty

- You could be charged with tax evasion - a felony

- Prison time: up to 5 years per count

Final truth: You can’t outsmart the system

Crypto was built on decentralization. But taxes? They’re centralized. And they’re getting smarter. The days of hiding crypto gains are over. The tools to catch you are already here. Do the right thing. Pay what you owe. Use legal strategies to reduce your bill. Keep records. Get help. Your future self will thank you - not for avoiding taxes, but for not risking everything to dodge them.Is it legal to not report crypto if I didn’t cash out?

No. The IRS taxes crypto as property. Selling, trading, or spending crypto triggers a taxable event - even if you didn’t convert it to cash. For example, using Bitcoin to buy a laptop counts as a sale. You owe tax on the gain from when you bought it to when you spent it.

Can I use a decentralized exchange to avoid taxes?

No. While DEXs don’t require KYC, your wallet address is still on the public blockchain. If you ever linked that wallet to a KYC exchange (like Coinbase), the IRS can trace your entire history. Tools like Chainalysis track these links. You can’t hide forever.

Do I owe tax on crypto I received as a gift?

You don’t pay tax when you receive crypto as a gift. But when you later sell it, you owe capital gains tax based on the original cost basis - not the value when you received it. If the gift was over $19,000 in 2025, the giver may need to file a gift tax return, but you still owe tax on any gain when you sell.

What if I lost my private keys? Do I still owe tax?

Yes. The IRS doesn’t accept “lost keys” as a reason to avoid tax. If you sold or traded crypto before losing access, you still owe tax on that gain. You can’t claim a loss unless you can prove the wallet is permanently inaccessible - and even then, it’s complicated and rarely accepted.

Will the IRS know if I didn’t report my crypto?

Yes. Starting in 2026, all U.S. exchanges must report your crypto trades on Form 1099-DA. The IRS already has data from past subpoenas. They cross-check bank deposits, wallet addresses, and tax returns. If your income doesn’t match your spending, they’ll investigate.

Can I file an amended return for past crypto years?

Yes. The IRS allows you to file amended returns (Form 1040-X) for up to three prior years. If you didn’t report crypto gains, correcting this now reduces your risk of penalties or audit. It’s better to fix it yourself than wait for them to find you.

Do I owe tax on crypto airdrops?

Yes. The IRS treats airdrops as ordinary income. You owe tax on the fair market value of the tokens when you received them. If you later sell them, you owe capital gains tax on any increase in value from that point.

What’s the safest way to handle crypto taxes?

Use a crypto tax software tool to track all transactions. Keep records of every buy, sell, trade, and reward. File your taxes accurately each year. If you’re unsure, hire a CPA who specializes in cryptocurrency. Avoid guesswork - compliance is your best protection.

Sam Daily

November 27, 2025 AT 08:36 AMBro, I just used my BTC to buy a gaming rig last month and thought I was slick 🤫 Turns out I just handed the IRS a gift certificate 😅 Good thing I caught this before tax season. Koinly saved my sanity.

Evelyn Gu

November 27, 2025 AT 19:59 PMI just... I just can't believe how many people think crypto is some kind of tax-free zone? Like, we're not in 2015 anymore. The blockchain is a public ledger. It's not magic. It's math. And the IRS? They're not dumb. They've got algorithms that can trace a wallet from a coffee shop to a yacht. I cried when I realized I owed $4k last year. But I paid it. And now I sleep better. Seriously. Don't be like me. Don't wait until you're panic-calling a CPA at 2am.

priyanka subbaraj

November 28, 2025 AT 11:28 AMThey're coming for you. The IRS. The blockchain. The algorithms. The auditors. The subpoenas. The prison stripes. You think you're hidden? You're not. You're a walking audit waiting to happen.

Tony spart

November 29, 2025 AT 04:06 AMLmao why are we even talking about this? The government wants to control everything. Crypto is freedom. If they want my money, they gotta come get it. I'm not some tax-paying sheep. 💪🇺🇸

Mark Adelmann

December 1, 2025 AT 03:44 AMHey everyone - just wanted to say this post is super helpful. Seriously. I'm new to crypto and was totally clueless. I used CoinTracker to import my trades and found I owed way more than I thought. But now I'm on track. If you're confused, just start tracking. No shame in learning. You got this.

ola frank

December 2, 2025 AT 11:41 AMThe ontological distinction between tax avoidance and evasion hinges on epistemic intent and procedural transparency. The IRS's interpretation under IRC § 61 and Rev. Rul. 2014-21 establishes crypto as property, thereby triggering capital gain recognition upon disposition. The emergence of Form 1099-DA institutionalizes blockchain forensics into federal compliance architecture - a paradigm shift in fiscal sovereignty. The notion of anonymity in decentralized systems is a ludic fallacy when cross-referenced with KYC on-ramps.

Angel RYAN

December 3, 2025 AT 21:25 PMHonestly, this is one of those posts that makes you pause. I used to think I could wing it. Now I use Koinly and file every year. It's not sexy, but it's peace of mind. No drama. Just done.

stephen bullard

December 5, 2025 AT 11:21 AMI used to think taxes were the enemy. Then I realized - the real enemy is fear. Fear of paperwork. Fear of paying. Fear of being called out. But here’s the secret: doing the right thing doesn’t make you a sucker. It makes you free. Free from stress. Free from nightmares. Free from wondering if today’s the day the IRS shows up. Do the work. You’ll thank yourself later.

SHASHI SHEKHAR

December 7, 2025 AT 04:11 AMBro, I just got airdropped 500 $SHIB last week 😍 And I was like, 'free money!' Then I read this and realized I owe tax on it already 😅 Used TokenTax to track everything. Now I’m chill. Pro tip: Always record the USD value when you receive crypto - even if you don’t sell! 📊💰 #CryptoTaxIsReal

Vaibhav Jaiswal

December 7, 2025 AT 16:52 PMI used to think I was a crypto genius. Then I lost $20k on a bad trade and realized I still owed taxes on the $50k I made earlier. The IRS doesn’t care if you lost money later. They care about what you reported. Lesson learned the hard way. Don’t be me.

Abby cant tell ya

December 8, 2025 AT 01:07 AMWow. So you're saying if I didn't report my 2021 gains, I'm basically a criminal? I just thought I was being smart. Guess I'm just a naive idiot. Thanks for the guilt trip.

Janice Jose

December 8, 2025 AT 18:07 PMI get why you're upset. But honestly? The fact that you're even reading this means you care. That’s half the battle. You can fix this. No one’s judging you right now. Just take the next step - open Koinly, import your history, and breathe. You’re not alone.

Savan Prajapati

December 10, 2025 AT 04:08 AMReport. Or get caught. Simple.